A lot of industry conversation assumes that environmental regulation and societal pressure automatically translate into rapid operating improvements. The data tell a more nuanced story.

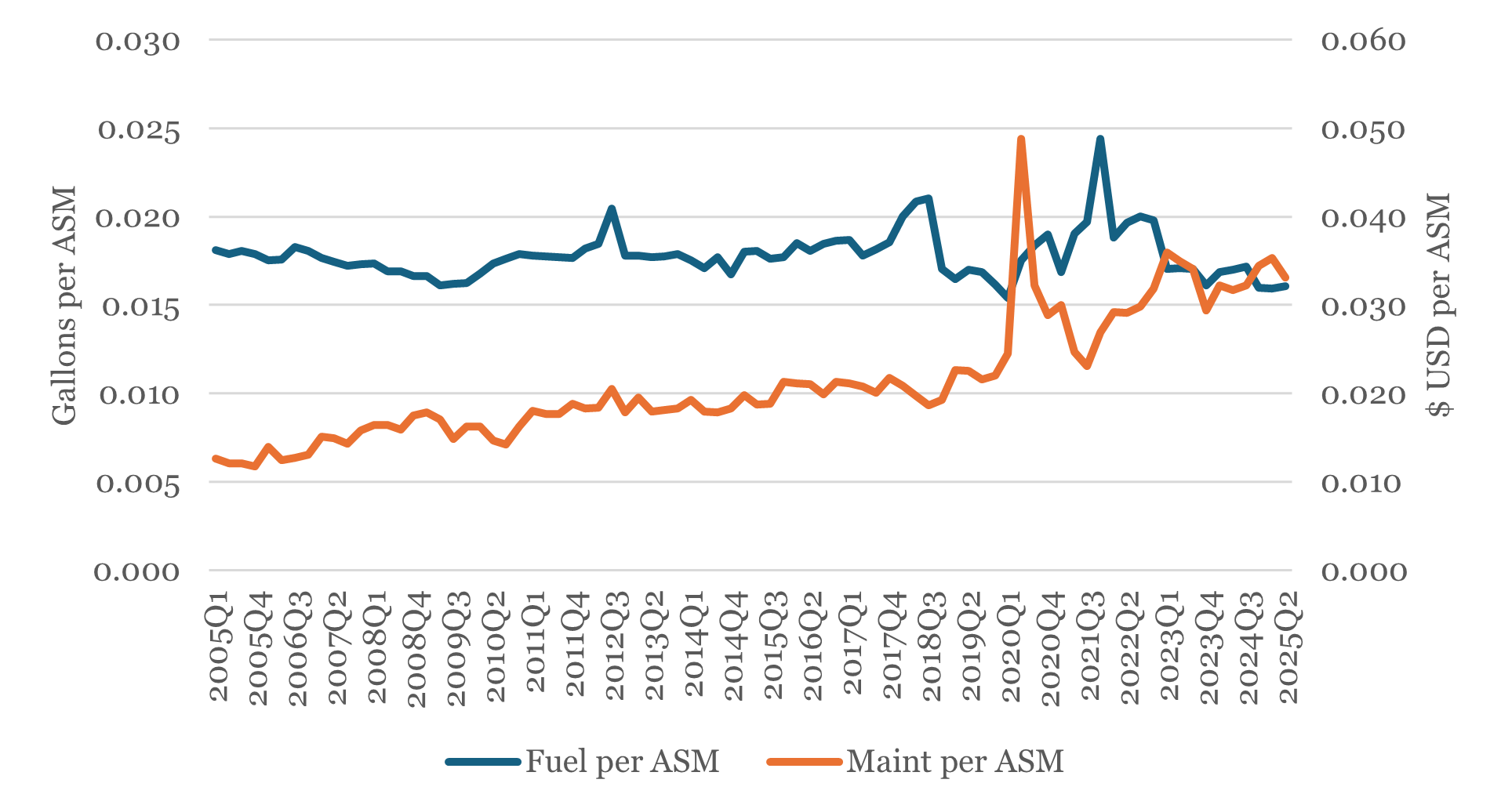

Across 20 U.S. carriers over 2005–2025, fuel consumption intensity improves only modestly and unevenly, while real maintenance expense shows a pronounced upward drift.

Why this matters

Fuel is the headline issue in sustainability discussions, but maintenance is quietly becoming a bigger part of the operating-cost reality. When fuel intensity barely improves while maintenance cost intensity rises, the economics of keeping aircraft in service shift, and so do financing and fleet decisions.

The cleanest way to measure it: per ASM, not per RPM

A key point is measurement. Per-RPM metrics can look worse during downturns simply because load factor falls, even if the airline did not become less efficient. ASM-based intensity measures avoid that mechanical distortion by relating fuel and maintenance to capacity deployed, not demand realized.

Business model differences are not subtle

When you compare fuel and maintenance intensity per ASM across carrier types, the pattern is consistent:

Regional and short-haul operators face the steepest squeeze

The most important operational takeaway is that regional airlines show little to no improvement in fuel intensity per ASM, alongside a pronounced increase in maintenance intensity.

In plain terms, short-haul flying is cycle-heavy, smaller-gauge aircraft are disadvantaged on a per-capacity basis, and the maintenance burden rises quickly as fleets accumulate cycles.

The market implication

If the industry’s fuel intensity improvements are gradual, but real maintenance costs keep climbing, stakeholders need to pay more attention to the maintenance side of the equation. For lessors, lenders, and investors, maintenance forecasting, reserve adequacy, and technical risk increasingly matter as much as the “green” narrative.

InfoJets note: We help clients connect aircraft specifics, maintenance reality, and market conditions to support valuation, financing, and transaction decisions. If you are evaluating an aircraft, lease, or portfolio, we are happy to help you frame the drivers that matter.

Across 20 U.S. carriers over 2005–2025, fuel consumption intensity improves only modestly and unevenly, while real maintenance expense shows a pronounced upward drift.

Why this matters

Fuel is the headline issue in sustainability discussions, but maintenance is quietly becoming a bigger part of the operating-cost reality. When fuel intensity barely improves while maintenance cost intensity rises, the economics of keeping aircraft in service shift, and so do financing and fleet decisions.

The cleanest way to measure it: per ASM, not per RPM

A key point is measurement. Per-RPM metrics can look worse during downturns simply because load factor falls, even if the airline did not become less efficient. ASM-based intensity measures avoid that mechanical distortion by relating fuel and maintenance to capacity deployed, not demand realized.

Business model differences are not subtle

When you compare fuel and maintenance intensity per ASM across carrier types, the pattern is consistent:

- ULCCs are the lowest intensity operators on both fuel and maintenance per ASM.

- LCCs fall between ULCCs and full-service carriers.

- Regional airlines have the highest intensities, consistent with shorter stage lengths and smaller aircraft gauge.

Regional and short-haul operators face the steepest squeeze

The most important operational takeaway is that regional airlines show little to no improvement in fuel intensity per ASM, alongside a pronounced increase in maintenance intensity.

In plain terms, short-haul flying is cycle-heavy, smaller-gauge aircraft are disadvantaged on a per-capacity basis, and the maintenance burden rises quickly as fleets accumulate cycles.

The market implication

If the industry’s fuel intensity improvements are gradual, but real maintenance costs keep climbing, stakeholders need to pay more attention to the maintenance side of the equation. For lessors, lenders, and investors, maintenance forecasting, reserve adequacy, and technical risk increasingly matter as much as the “green” narrative.

InfoJets note: We help clients connect aircraft specifics, maintenance reality, and market conditions to support valuation, financing, and transaction decisions. If you are evaluating an aircraft, lease, or portfolio, we are happy to help you frame the drivers that matter.